- 5 min read

A Complete Guide to Medicare Enrollment: Everything You Need to Know

Medicare enrollment is a critical milestone in your healthcare journey, but the process doesn’t have to be overwhelming. Whether you’re approaching 65 or helping a loved one navigate their Medicare options, understanding when and how to sign up for Medicare can save you from costly penalties and ensure you have the coverage you need when you need it.

Finding the right time to enroll in Medicare is a delicate balance. Enrolling too early could leave you spending money you don’t need to while signing up too late will have you paying lifelong penalties. While you may be eligible for Medicare at 65, that doesn’t always mean you have to sign up for Medicare. Learn more about the best time to enroll in Medicare, who can delay enrollment, and the enrollment periods you need to know.

Understanding Medicare Registration Basics

Before diving into how to apply for Medicare benefits, it’s essential to understand that Medicare isn’t a one-size-fits-all program. The program consists of multiple parts, each covering different aspects of your healthcare needs. When you begin the medicare registration process, you’ll need to consider whether you need Part A (hospital insurance), Part B (medical insurance), Part D (prescription drug coverage), or a Medicare Advantage plan.

Social Security Medicare enrollment is automatically triggered for some individuals, particularly those already receiving Social Security benefits before age 65. However, if you’re not receiving Social Security benefits, you’ll need to take active steps to register for Medicare.

When Should I Sign Up for Medicare Benefits?

The timing of your Medicare enrollment depends largely on your current employment and insurance situation. Here’s a comprehensive breakdown of various scenarios:

Working Past 65

Your employer’s size plays a crucial role in determining when you should enroll. If you or your spouse work for a company with 20 or more employees on payroll, you have options:

You can delay enrollment without penalty because your employer coverage is considered “creditable.” When you eventually retire or lose coverage, you’ll qualify for a Special Enrollment Period.

However, some people choose to enroll in Part A at 65 even while working since it’s usually premium-free and can serve as secondary insurance to your employer coverage.

For those working at companies with fewer than 20 employees, enrollment at 65 is mandatory, as Medicare becomes the primary payer, and your employer insurance shifts to secondary status.

COBRA and Medicare Interaction

If you’re on COBRA insurance, the rules are different and require careful attention. You must enroll in Medicare when you turn 65, even if your COBRA coverage hasn’t expired.

COBRA becomes the secondary payer once you’re Medicare-eligible, meaning you’ll be responsible for costs that Medicare would have covered if you had enrolled. Additionally, COBRA doesn’t qualify as creditable coverage, so delaying enrollment could result in permanent penalties.

TRICARE Beneficiaries

Military personnel and their families with TRICARE face specific requirements. At age 65, enrollment in Medicare becomes mandatory because TRICARE transitions to TRICARE For Life, which works exclusively as a Medicare supplement. Without Medicare Parts A and B, you could lose your TRICARE coverage entirely.

ACA Marketplace Plans

Those with Affordable Care Act (ACA) marketplace plans should transition to Medicare at 65 because tax subsidies and cost-sharing benefits end at Medicare eligibility. Full-price premiums often make ACA plans more expensive than Medicare, and you can’t receive premium subsidies from both Medicare and the ACA simultaneously.

Ready to talk to a guide?

Book a free call by clicking below or if you are free now give us a call at: 800.8648890

How to Sign Up for Medicare: Available Enrollment Periods

Understanding Medicare’s various enrollment periods is crucial for timely medical insurance coverage and avoiding penalties.

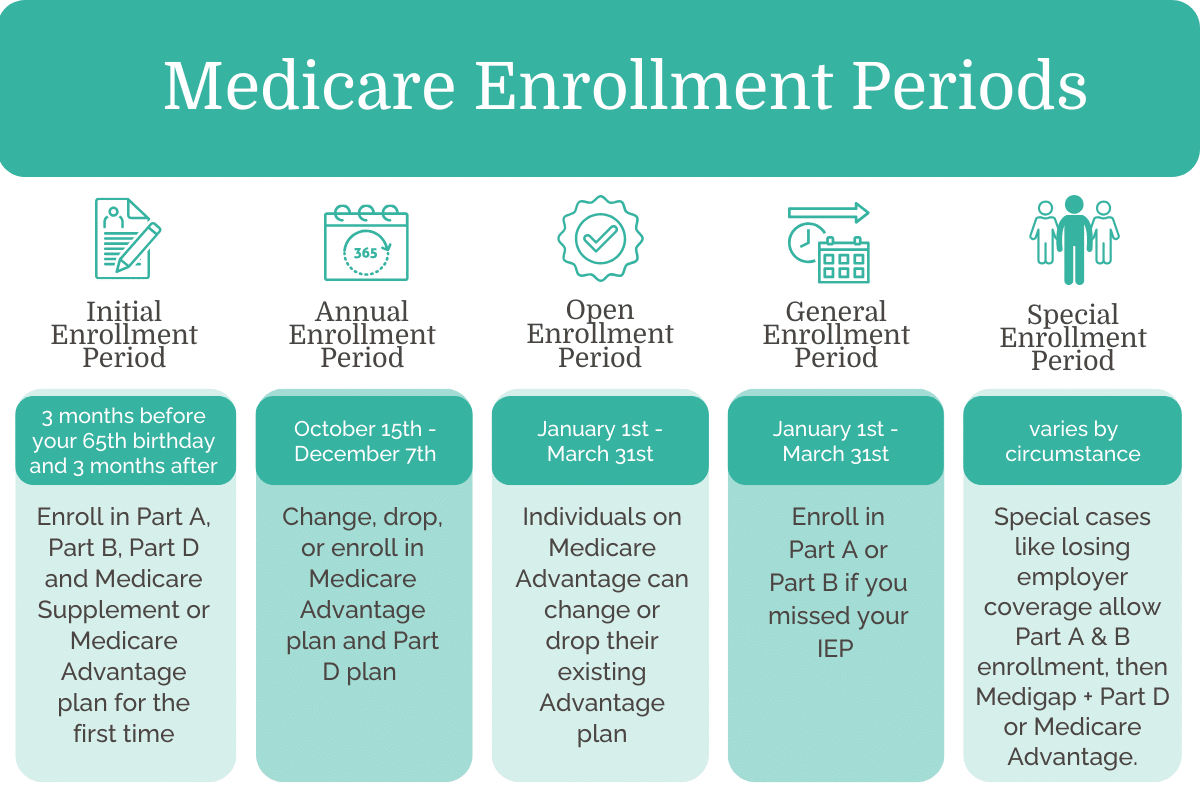

Initial Enrollment Period (IEP)

Your Initial Enrollment Period spans seven months, including three months before your 65th birthday month, your birthday month, and three months after.

This period is particularly important because:

It’s the optimal time to enroll in Medicare Part B without penalties

You can get guaranteed issue rights for Medicare Supplement plans

You have access to all available medical insurance options without restriction

Special Enrollment Period (SEP)

Special Enrollment Periods accommodate various life changes and circumstances, including:

Employment changes

Loss of employer coverage

Relocation outside your plan’s service area

Changes in institutional status

The length of your SEP varies by qualifying event, ranging from two to eight months. To utilize an SEP, you’ll need to provide documentation proving your eligibility.

General Enrollment Period (GEP)

Running from January 1st through March 31st annually, the General Enrollment Period serves as a safety net for those who missed their IEP. However, be aware that:

Medical insurance coverage begins on the first day of the month following your application. For example, if you apply in January, coverage starts on February 1st. If you apply in February, it starts on March 1st. If you apply in March, it starts on April 1st, and that is the last opportunity until the next year.

Late enrollment penalties may apply

You might face gaps in coverage

Annual Enrollment Period (AEP)

The Annual Enrollment Period, often called Medicare Open Enrollment, runs from October 15th through December 7th. During this time, you can:

Switch between Original Medicare and Medicare Advantage

Change Medicare Advantage plans

Modify prescription drug coverage

Make updates to take effect January 1st

Advantage Open Enrollment Period

If you’ve heard of the Medicare Advantage Open Enrollment Period, know it’s the same as the Medicare Annual Enrollment Period.

Can I Sign Up for Medicare Online?

Yes, online enrollment is available and often preferred for its convenience. The Social Security Administration handles Medicare registration through their website, where you can:

Complete your initial enrollment

Apply for Medicare Parts A and B

Manage your existing coverage

Update personal information

The online application process typically takes less than 30 minutes, requiring basic personal information, employment details, and current insurance information.

Common Medicare Enrollment Mistakes to Avoid

Making informed decisions about Medicare enrollment requires understanding potential pitfalls. Here are some common Medicare mistakes that can lead to coverage gaps or unnecessary expenses:

Assuming Medicare Covers Everything

Original Medicare (Parts A and B) doesn’t cover all healthcare services. Many people are surprised to learn that routine dental care, vision services, hearing aids, and most long-term care services aren’t covered. Understanding these limitations early helps you:

Speak to a licensed advisor about your options for additional coverage

Budget for out-of-pocket healthcare expenses

Make informed decisions about supplemental coverage

Misunderstanding Part D Enrollment

Prescription drug coverage through Medicare Part D has its own enrollment rules and penalties. Many people make the mistake of:

Waiting to enroll because they don’t currently take medications

Failing to verify whether their existing drug coverage is “creditable”

Not comparing Part D plans annually during open enrollment

The late enrollment penalty for Part D is permanent and increases the longer you go without creditable drug coverage after becoming eligible.

Medicare Enrollment for Special Situations

While most people enroll in Medicare at age 65, certain circumstances can affect your enrollment timing and options.

Disability-Based Medicare Enrollment

If you’re under 65 and receiving Social Security disability benefits, you may qualify for Medicare after a 24-month waiting period. Important considerations include:

Automatic enrollment after the waiting period

Different timing for Initial Enrollment Period Special rules for certain conditions like ALS or End-Stage Renal Disease

Potential need for supplemental coverage, as some Medicare Supplement plans may not be available until age 65

International Residents and Medicare

For U.S. citizens living abroad, Medicare enrollment requires careful consideration:

Medicare generally doesn’t cover healthcare services outside the U.S.

Delaying enrollment while living abroad could result in late penalties.

Special enrollment periods may apply when returning to the U.S.

The need to coordinate coverage with local healthcare systems.

Those planning to live or travel extensively abroad should carefully evaluate their Medicare enrollment timing and supplemental coverage needs to ensure adequate healthcare protection both at home and abroad.

Preparing for Enrollment

To ensure a smooth enrollment process:

Review your current health insurance and understand how it will interact with Medicare

Gather necessary documentation, including proof of citizenship and employment records

Consider your healthcare needs and budget

Research Medicare Advantage and Supplement plans available in your area

Consult with a licensed advisor for personalized guidance

Prepare for Medicare Enrollment with Medicare School

Navigating Medicare enrollment can feel overwhelming, but Medicare School is here to help. We can help you understand your eligibility so you can find the right time to enroll in Medicare based on your situation.

At Medicare School, we are passionate about helping you understand Medicare so you can enjoy retirement. Browse our blog or check out our YouTube channel to learn more about Medicare and Social Security. You can also enroll in our free Medicare Workshop or download our “Complete Guide to Medicare” for a crash course on Medicare before you enroll.