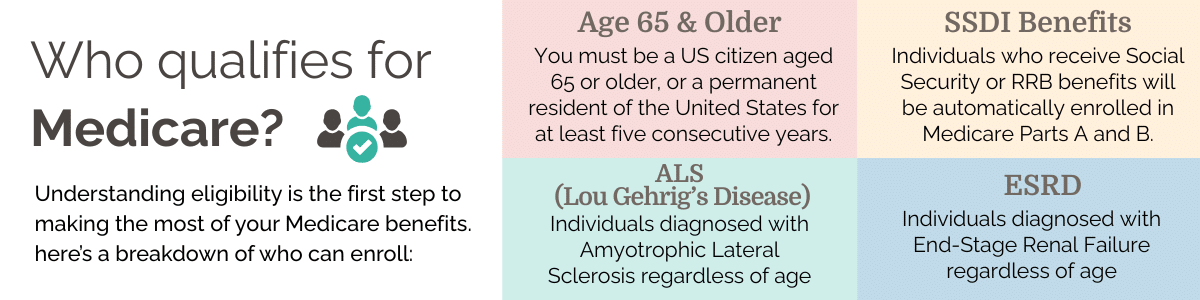

Who is Eligible for Medicare?

Updated Medicare Costs for 2026

We’re currently filming an updated video for this page. While that’s in progress, you can reference the correct Medicare cost information for 2026 below.

Costs shown are standard 2026 Medicare amounts and may change annually.

Updated Medicare Costs for 2026

We’re currently filming an updated video for this page. While that’s in progress, you can reference the correct Medicare cost information for 2026 below.

Costs shown are standard 2026 Medicare amounts and may change annually.

Understanding Medicare Eligibility: A Comprehensive Guide

Welcome to your daily dose of Medicare education. Today, we delve into the critical question that many have: who is eligible for Medicare? All too often, people are left confused about how this governmental health insurance program works, who qualifies for it, and what conditions they have to meet. This post aims to dispel the obscurity around this topic, offering a detailed insight into the criterion for Medicare eligibility.

Eligibility: The 40 Quarter Rule

At the heart of Medicare’s eligibility requirements lies the 40 Quarter Rule. But what does this mean?

Medicare eligibility is primarily dependent on you having 40 quarters (or 10 years) of Medicare taxes paid into the system. The necessary condition here is 40 quarters. Once you have paid taxes for these 40 quarters into the system, you qualify to reap Medicare benefits and, importantly, Social Security as well.

Key Point: The determining factor for Medicare eligibility is having 40 quarters of tax payment into the system.

Once you satisfy this necessary condition, you can access Medicare Part A at no cost. This applies universally, regardless of how much or how long you have worked beyond these 40 quarters, and it also entitles you to Medicare Part B benefits. Before celebrating, it’s important to note that most beneficiaries will need to pay a premium for Medicare Part B.

Drawing Benefits From a Spouse

What if you haven’t fulfilled the 40 quarter condition on your own? Medicare has provisions for this as well. Your lack of 40 quarters does not disqualify you from the scheme; instead, the system allows you to draw benefits from a spouse.

Let’s examine the specifics.

For a current spouse, the requirement is that you must be married for at least one year. In this case, your spouse does not need to be receiving Social Security; but they must be eligible for it, meaning they should be at least 62 years old. For example, if you’re 65 and your spouse is 58, you cannot draw the 40 quarters from their work record until they reach 62.

Drawing From an Ex-Spouse

What about those who were previously married and no longer have a spouse? Can they qualify for Medicare benefits? The answer is indeed yes!

If you were married previously, you could draw benefits from your ex-spouse. Here are the guidelines:

You must have been married to your ex-spouse for a minimum of ten years.

You should not have remarried before the age of 60.

If you did remarry after the age of 60, or that second marriage ended (through death or divorce), you can go back to your ex-spouse’s work record and draw the 40 quarters.

Just like in the case of a current spouse, your ex-spouse must also be at least 62 years old for you to receive benefits from their record.

Remember the golden rule: having 40 quarters of your own or off someone else’s work record.

How to Apply

Now, if you have to draw off someone else’s work record, there is a specific procedure that you need to follow:

This application cannot be done online. You have to make an appointment at your local Social Security office to enroll in Medicare.

Understanding the eligibility criteria for Medicare can seem daunting. But, armed with these insights, you’re now better placed to navigate the system and understand your options. In our next post, we’ll take a detailed look at positioning you for successful enrollment in Medicare.

Get the Right Medicare Plan For You

Book a Consultation Below &

Here Is What You Can Expect:

Enroll correctly & avoid penalties.

Avoid selecting a plan with limited coverage and surprising out-of-pocket expenses.

Receive unbiased advice from our independent guides that work for you, not an insurance company.

What to expect from a Medicare School consultation:

- Enroll correctly which means you avoid penalties.

- Understand your coverage so you aren’t surprised by any unexpected out-of pocket expenses.

- Avoid selecting a plan with limited coverage which means you can be confident in your decision.

- Save time with our simplified process so you can spend more time doing what you enjoy.

- Receive unbiased advice from our independent guides that work for you, not an insurance company.

Words from our clients

A few of the 150,000 people we have helped.

At MedicareSchool.com, we empower you with the knowledge and guidance you need to get the best Medicare plans and live retirement worry-free.